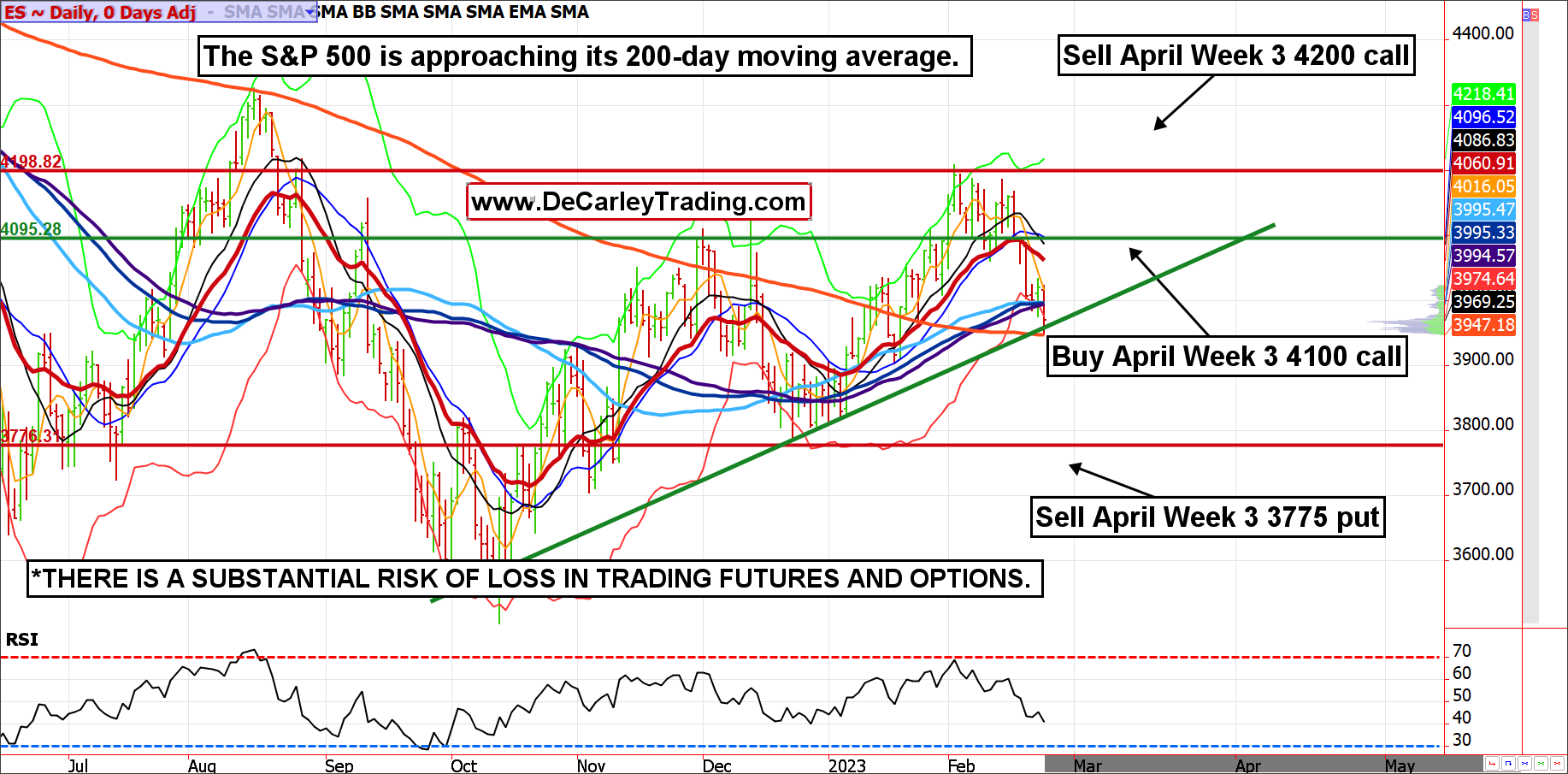

The E-mini S&P 500 tested its 200-day moving average and appears to be holding. Despite a rocky week for the stock indexes, the overall trend remains higher (daily trendlines are pointing up and trendline support is holding).

Of course, the overwhelming media narrative is one of bearishness for stocks but with so much sidelined cash looking for a place to go and the masses positioned for lower equities, the pain trade is likely higher (markets have a tendency to cause the most amount of pain to the majority of market participants).

That said, we realize markets are dicey near significant technical pivot levels; thus, it is important to leave plenty of room for error. One way to “get long” the market with little out-of-pocket expense and risk placed beneath distant support levels is a bull call spread with a naked leg. This strategy is intended to use the market’s money to pay for a long call option, but the catch is there is unlimited risk.

We like using the April week three options and prefer to construct the spread in favor of premium collection as opposed to profit potential. Specifically, we like buying the April E-mini S&P 500 4100 call, selling the 4200 call, and selling the 3775 put. The risk at expiration comes below 3775, which is intentionally below the last swing low and probably isn’t a bad place to get long futures from if it comes to the option being assigned.

Thus, if the uptrend remains mostly intact, this trade should perform relatively well.

If the June E-mini S&P is between 3775 and 4100 at expiration, the trade makes the premium collected (about $700), but the profits pick up between 4100 and 4200 with the best-case scenario being the June E-mini is above 4200 at expiration. If held to the end, the profit would be about $5,700.

Chart Source: QST

Alternative Strategy

This spread can be done with micro E-mini S&P 500 options; this cuts the risk, margin, and stress to 1/10th the size.

Similarly, those looking for simplicity might consider simply going long a micro E-mini futures contract. At $5 per point and a contract value of about $20,000 the risk is relatively manageable for most traders regardless of account size.

*Aggressive Trade Idea: Bull Call Spread With a Naked Leg in April E-mini S&P 500

— Buy April ES 4100 Call

— Sell April ES 4200 Call

— Sell April ES 3775 Put

Total Premium Collected = About 14.00 points cents, or $700 minus transaction fees

These options expire on April 21, with 55 days to expiration

Rand = $ 7,250

Risk = Unlimited below 3775

Maximum Profit = $5,700 before considering transaction costs if the June E-mini S&P 500 is above 4200 at expiration

*There is a substantial risk of loss in trading futures and options. There are no guarantees in speculation; most people lose money trading commodities. Past performance is not indicative of future results.

Kritt eng E-Mail Alarm wann ech en Artikel fir Real Money schreiwen. Klickt op de "+ Follow" nieft menger Byline zu dësem Artikel.

Source: https://realmoney.thestreet.com/investing/options/an-aggressive-s-p-play-get-long-the-market-with-little-out-of-pocket-expense-16116880?puc=yahoo&cm_ven=YAHOO&yptr=yahoo